For car shoppers in the United States, the “lease vs. buy” decision in early 2026 is less about what’s universally cheaper and more about which risks you want to carry: depreciation risk, interest-rate risk, and flexibility risk. New-vehicle prices remain historically high – January 2026’s average transaction price was about $49,191 – and incentives have pulled back versus late 2025, even as lender rates and APRs show signs of easing rather than collapsing.

Leasing can still make strong sense if you value a lower and more predictable monthly payment, drive within typical mileage limits, and like upgrading every 2–3 years – especially in segments with strong residual values or unusually high incentives (EV incentives remain well above the overall market average).

Buying tends to win when you drive a lot, keep cars for many years, or want full control over the vehicle (mods, usage, resale timing). It also becomes more compelling if you can reduce borrowing costs (bigger down payment, shorter term, or paying cash) and avoid the negative-equity cycle that’s increasingly common for frequent trade-ins.

Market context in 2026

The starting point in 2026 is affordability pressure. The latest Kelley Blue Book reporting (published through Cox Automotive) puts the average new-vehicle transaction price at $49,191 in January 2026, with the average MSRP at $51,288 – and MSRPs staying above $50,000 for 10 straight months.

Incentives matter because they directly change whether leasing feels “cheap” or “meh.” In January 2026, the average incentive package was reported at 6.5% of ATP (roughly $3,200), down from December’s 7.5% and below year-ago levels. That doesn’t mean deals disappeared – it means you have to be more selective about models and timing.

On the borrowing side, rates remain elevated. Commercial-bank new-auto loan rates were around the mid–7% range on common terms in the latest available data (e.g., ~7.5% for 48- and 72-month new-auto loans as of November 2025), and consumer-facing APRs remained high in late 2025 even with modest easing.

That shows up in payments. Edmunds reports the average monthly payment for financed new-vehicle purchases hit $772 in Q4 2025, with an average APR of 6.7% and longer loan terms still doing heavy lifting.

Used-car pricing is one of the few relief valves. Inflation measures show “used cars and trucks” prices rolling over: the year-over-year change was -2.0% in January 2026 in consumer price data sourced from the U.S. Bureau of Labor Statistics and published via FRED. That can tilt the equation toward “buy (especially used)” if you’re open on model year and features. Finally, leasing itself remains a meaningful channel but not as dominant as it was in some pre-pandemic years. Cox Automotive’s 2026 outlook projects overall lease penetration at about 21% (down from 2025), reflecting a market where incentives, EV policy changes, and inventory normalization are all in flux.

The financial comparison that actually matters

Most shoppers compare lease vs. buy by monthly payment alone. That’s understandable – but it’s incomplete. A better comparison is total cost of ownership (TCO) over your holding period (2–3 years for many leasers, 5–10 years for many buyers), plus the value of flexibility.

Lease vs. buy cost drivers, translated

Depreciation – Buying: You absorb the vehicle’s actual depreciation, but you can “dilute” it by keeping the vehicle longer. Edmunds’ ownership-cost guidance notes new cars commonly lose a substantial portion of value in the first years; depreciation is often the biggest single cost category.

- Leasing: You’re essentially pre-paying expected depreciation (the spread between negotiated price and residual value) over the term, plus finance charges. If the vehicle holds value better than expected, the leasing company benefits – unless you buy it at lease end. If it holds value worse than expected, your downside is partly capped (again, unless you buy).

Financing / interest – Buying: In Q4 2025, APR averaged 6.7% for new-vehicle financing, with many borrowers stretching terms. High interest makes “long loans + early trade-in” especially dangerous.

- Leasing: Leasing charges interest too – just expressed as a “money factor.” Edmunds’ leasing basics explain the money-factor concept and warn that dealers may mark it up.

Taxes and fees – Buying: Typically includes sales tax (state-dependent), registration, title, documentation, and any dealer add-ons.

- Leasing: You’ll usually see an acquisition fee up front (Edmunds cites $595–$1,095 as a typical range) and often a disposition fee at the end (commonly $300–$400).

- Taxes vary by state. A concrete example: in California, AnyAutoLeasing’s guide notes sales tax is charged on each monthly lease payment (not the full vehicle price) and local rates can be high in some counties.

Insurance – Buying: Lenders generally require comprehensive/collision while you’re financed, but coverage requirements can vary by lender and borrower profile.

- Leasing: The leasing company typically dictates the insurance coverage you must carry, so you should price insurance before you sign.

The “equity” reality – Buying: You can build equity if the loan balance falls faster than the car’s value falls. But the opposite – negative equity – is increasingly common. Edmunds reports 29.3% of trade-ins toward new-vehicle purchases had negative equity in Q4 2025, with the average amount owed on underwater trade-ins reaching $7,214.

- Leasing: You generally don’t build equity unless (a) you put cash down (usually not recommended on leases) or (b) the vehicle ends up worth more than the residual and you exercise a buyout.

A small comparison table

| Factor | Leasing | Buying |

| What you’re paying for | Depreciation used during term + rent/finance charge + fees/taxes | Full vehicle price (cash or loan) + taxes/fees, then you own an asset |

| Monthly payment tendency | Often lower (not always) | Often higher, especially at today’s APRs |

| End-of-term | Return, extend, buy, or re-lease | Keep, sell, trade any time |

| Depreciation risk | Partly shifted to lessor (unless you buy) | Fully on you (but you can offset by keeping longer) |

| Common surprise costs | Mileage overage, wear-and-tear, disposition fee | Negative equity on early trade-in, repair costs out of warranty |

| Best when | You want predictable costs and frequent upgrades | You keep cars long-term or drive high mileage |

How to compare deals without getting tricked

If you want a real apples-to-apples comparison, use these two metrics:

Effective monthly cost of a lease

(Monthly payment × months) + due-at-signing + expected end fees (like disposition) ÷ months

This forces you to look beyond the headline payment. Any AutoLeasing emphasizes that a low payment with a big down payment can be misleading, and encourages comparing total lease cost and drive-off costs – not just the monthly number.

Net cost of buying over your ownership window

(Down payment + total loan payments + taxes/fees + insurance difference + maintenance/repairs) − resale/trade-in value

This is why TCO tools matter: they remind you to include taxes, insurance, and maintenance/repairs, not just principal and interest.

Non-financial tradeoffs that can outweigh the math

Financials are only half of the decision. The other half is how you live with the vehicle and how often life changes.

Mileage and wear-and-tear discipline

Most standard leases are built around mileage caps (often 10,000–15,000 miles/year), and exceeding the cap can be expensive. Kelley Blue Book notes overage penalties often range from about $0.12 to $0.30 per mile, and AnyAutoLeasing’s Los Angeles guide gives a similar practical range (roughly $0.15–$0.30 per mile) while emphasizing that underestimating mileage is a common mistake

Flexibility and exit options

Leases are contracts. Ending a lease early can be costly, and it’s not as simple as “return it whenever.” KBB’s leasing guide is blunt that early termination can require significant penalties, while lease-return guidance encourages planning ahead and understanding end-of-lease charges.

Buying, by contrast, gives you the option to sell anytime – but you may be constrained by negative equity if your loan balance is high relative to the vehicle’s value.

Maintenance and warranty coverage

Lessee responsibility is real: you’re expected to follow the maintenance schedule and return the vehicle without excessive wear. The upside is that many leases end while the car is still relatively new, and KBB notes some new vehicles include free maintenance plans.

Buying shifts the long-term maintenance/repair uncertainty to you, which becomes more relevant if you keep a vehicle deep into out-of-warranty years.

Technology turnover and safety upgrades

If you like having the latest driver-assistance tech, leasing can align with faster upgrade cycles. The National Highway Traffic Safety Administration highlights that its 5-Star Safety Ratings program evaluates vehicles through frontal, side, and rollover tests and points consumers to recommended driver-assistance technologies that meet performance tests.

Buying doesn’t block you from newer tech – but it often means you’re living with the same hardware/software suite longer.

Who leasing or buying tends to fit best in 2026

The “right” choice usually becomes obvious when you match the option to your driving pattern and time horizon.

Leasing tends to fit best if…

You have predictable mileage and you like to change cars every 2–3 years. Lease structures (residual value + money factor) are designed around that replacement rhythm, and AnyAutoLeasing’s 2026 lease-deal guide argues that the best outcomes come from comparing multiple offers and focusing on lease structure – not just the advertised payment.

Leasing can also be attractive if you want payment predictability while prices remain high and incentives vary by segment (with EV incentives still above the market average as of January 2026).

Buying tends to fit best if…

You plan to keep the car well beyond the typical lease term – especially 6+ years. That’s where ownership can start compounding in your favor: you’re no longer making payments, and you’re not restarting the highest-depreciation portion of the curve every few years. The TCO framework reinforces why holding period matters because depreciation, financing, and repairs vary across time.

A special warning for frequent “buyers” who trade in every few years

If you buy but behave like a leaser (trade in around year 3), you can get the worst of both worlds: high depreciation and exposure to negative equity. Edmunds’ Q4 2025 data shows negative equity is both widespread and rising in magnitude, making early trade cycles riskier in today’s rate-and-price environment.

When the answer is “it depends – run both”

If your monthly budget is tight but your mileage is high (or uncertain), you may need to compare:

- a higher-mileage lease option vs.

- buying used (since used prices have shown easing in inflation data) vs.

- buying new with a shorter loan term to avoid long interest exposure.

Practical tips and a decision path you can use today

Below are practical moves that consistently improve outcomes in 2026 – regardless of whether you lease or buy.

Tips – Start with your real annual mileage, not your optimistic mileage. Mileage caps are where “good leases” become expensive; overage fees add up fast.

- Compare “total lease cost,” not just the monthly payment. AnyAutoLeasing highlights how low advertised payments can be driven by inflated due-at-signing or unrealistic mileage.

- Negotiate the vehicle price (cap cost) as if you were buying. Edmunds’ leasing basics emphasizes cap cost is negotiable and should be treated like the selling price.

- Keep lease down payments (cap cost reductions) minimal. Edmunds warns that cap cost reductions are generally not reimbursed by insurance if the vehicle is totaled, which makes large lease down payments riskier.

- Ask about the non-negotiables upfront. Acquisition fees often fall in a predictable range, residual values are generally set by the lender, and disposition fees are common – so get them in writing early.

- Time your shopping. AnyAutoLeasing’s 2026 deals guide points to month-end/quarter-end and model-year changeovers as moments when pricing can improve.

- If you buy, avoid the negative-equity trap. The data show that rolling debt forward can raise payments and limit your next options – so prioritize shorter terms, meaningful down payments, and vehicles that hold value if you expect to trade in.

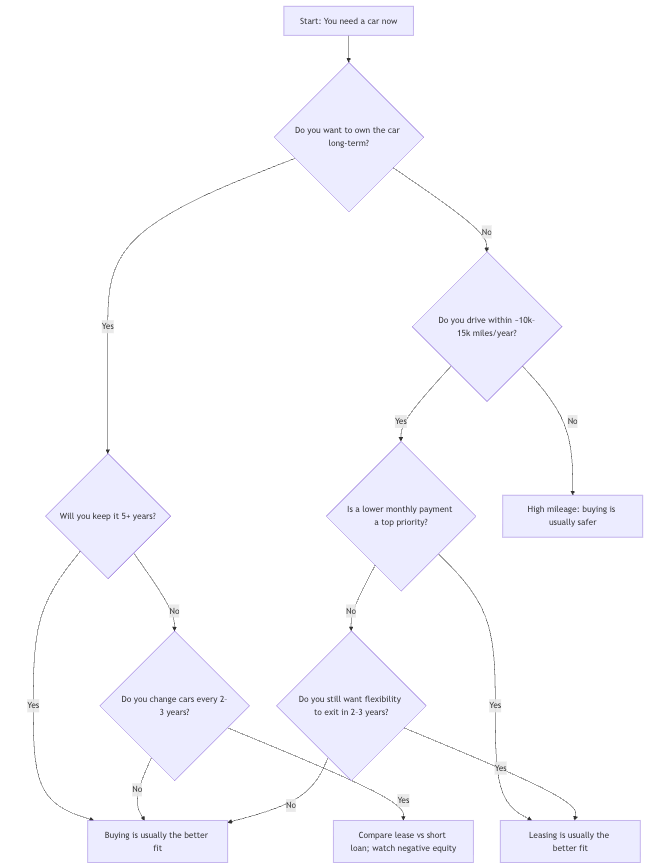

Decision flowchart (simple lease vs buy path)

In 2026, leasing is most rational when you value predictable costs and frequent upgrades and your mileage fits the contract structure – especially where incentives and residuals create strong “payment math.”

Buying is most rational when you keep vehicles longer or drive a lot, because you can outlast the steepest depreciation years – and you avoid recurring lease fees and mileage constraints.

If you buy but trade frequently, treat negative equity as the key risk to manage in today’s high-price, still-elevated-rate environment.